The Need for Technological Innovation in Business

There are several frameworks structured by management theorists to assess whether a business will be able to survive in the long run or not. From financial heuristics like a business’ capacity to reinvest in itself to more market-oriented thumb-rules like competitive differentiation – many factors go into forecasting which businesses stay consistently profitable over the long run. Innovation or being a part of market-changing innovation is a strong predictor of how long the business will stay sustainably profitable.

- Nokia and the Smartphone Revolution

Nokia was established as a pulp-mill in 1871. As it kept reinventing itself over the years, it became one of the largest telecommunication device developers, manufacturers, and sellers. Nokia sold computers, phones, pagers, and several other key pieces in the telecommunication infrastructure value chain. That was the key reason why Andy Rubin, the founder of Android, wanted his new operating system to be a part of the Nokia-ecosystem.

However, Nokia had other plans. Between 2008-2012, Nokia hardly reacted to the hyper-growth attained by the Google-Android partnership. Eventually, as it saw market share slipping, it partnered with Microsoft. It took several years and failed campaigns to bring Nokia to its lowest valuations in recent history. Today, Nokia is operational but exists in a much smaller form than it once used to.

The primary reason for Nokia’s decline was not rejecting some new-age startup called Android but rejecting the notion of third-party applications available on the company’s OS. Nokia made its own OS and then used its own apps to provide functionalities. Android tilted the model on its head by bringing the third-party app-store revolution to the masses, alongside Apple. Eventually, Nokia missed the boat and paid the due price by not getting to participate in the consistent rally of profits in the smartphone business.

The insurance industry is going through a similar revolution with telematics, pay-per-users variants, and big-data integrations. Some insurance companies have taken matters in-house while others are partnering with comprehensive technology platforms like Kruzr.

An insurance company that wants to be a part of the more efficient insurance industry, being for the very near future, will have a telematics program powered by competitive technology that makes insurance more affordable for the customers without compromising on the coverage.

- Mission Insurance Company and the Risk Management Revolution

In the 1980s, Mission Insurance was operating one of the largest insurance platforms in the United States. The company was one of the leaders in the workers’ compensation segment, and from the looks of it, was positioned for growth. With its strong franchise and profitable core business, there was no reason for the company to work on liquidation or insolvency plans.

However, back then, many insurance companies were not running optimally managed risk management practices. Since they had significant market intelligence and economies of scale in the core business, many companies like Mission Insurance Company were able to stay profitable for years in their core verticals. As the company started expanding into other insurance products, it faced quick and deepening financial troubles.

Mission backed several unprofitable ventures and took reinsurance risk with third-party insurance products. Since the company did not have a robust risk management framework, it found itself in the middle of long-term liabilities that went way beyond the company’s earnings. Eventually, the company had to file for bankruptcy, and the proceedings lasted for more than 25 years. Many lenders got less than 40% of what the company owed them.

Technology solutions like Kruzr can help modern-day insurance companies avoid a similar trajectory. Since the core insurance market is getting competitive and profits are eroding, it is natural for insurance companies to expand into new products. Kruzr can help the insurance companies add new products like pay-per-use, which essentially operate in the same market economics but cater to a new segment of consumers who seek affordable and yet comprehensive insurance. The entire platform operates on the prowess of data analytics, designed to measure risk parameters in the real world – predictive risky behavior, big-data inputs on traffic & weather conditions, as well as driver nudging to mitigate driving inaccuracies.

- Transit Casualty Co. and the Need for Expansion

Transit Casualty Co. was found in 1945 and came with an innovative product line – it insured buses and public transit systems. While the product was innovative and there was a considerable market, Transit soon started expanding into verticals not naturally cohesive with its platform.

The company insured several businesses across the globe – dumping yards, breast implant makers, haulers, and tobacco companies. The company was dependent on insurance brokers to run its insurance policies into the market. Since its model kept a layer of agents between the company and the businesses buying the insurance policy, Transit never had a deep understanding of what market it was expanding into.

As a matter of fact, when the insolvency committee went to the Transit HQ, they couldn’t find most of the documentation for the policies that drove the company into bankruptcy. The company expanded into several product-lines and did so using entirely third party-driven solutions.

At its core, Transit failed to keep track of data. Many other companies had a similar model of working with associates, partners, and brokers. Most of them did not go bankrupt. Transit wanted to drive its entire business on autopilot, without having the checks & balances in place.

Kruzr ensures that your automobile insurance products are not running on proxy or third-party data. All the data aggregation happens at the customer-level, and the risk metrics hence calculated, are an accurate assessment of what you will owe if the claims are put in place. Since this happens in real-time with great sensitivity to economic, behavioral, and large-scale parameters, even when you introduce new products like pay-per-use, you have a strong grip on the risks you are undertaking.

Telematics and Innovation in the Insurance Industry

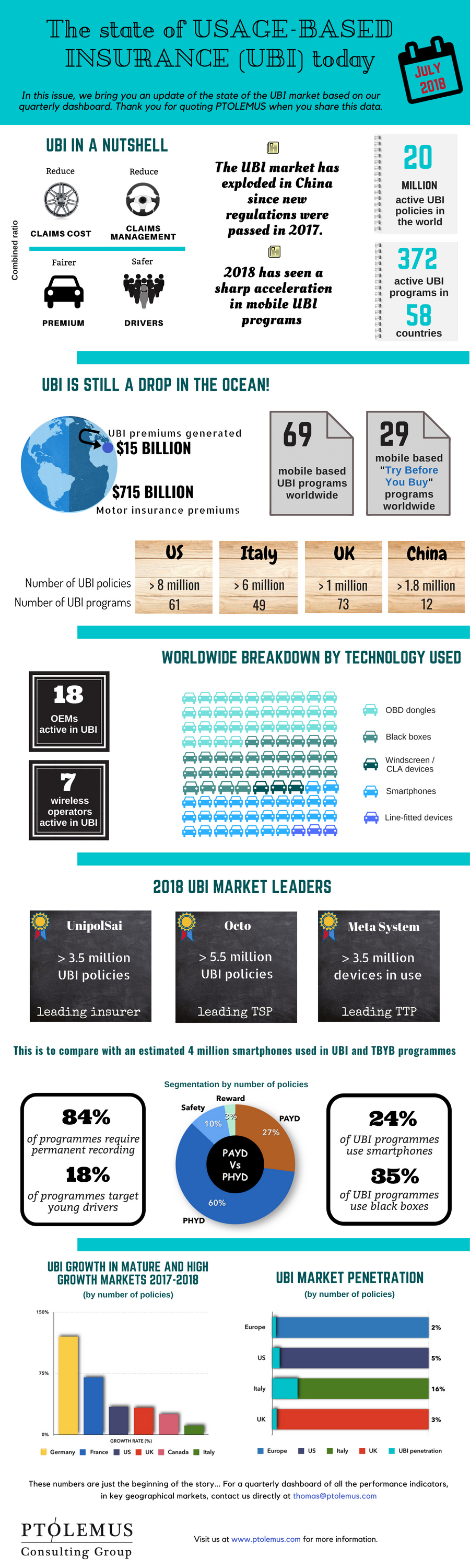

What android did to the smartphone business, telematics, and data analytics are doing to the insurance business. The market data speaks for itself:

- UBI is Already On-Track for a Major Thrust in Global Adoption.

Usage-based insurance has started accumulating global traction. Since more companies are operating with relatively more data, they have a clear understanding of the headwinds in the market. That is the reason why a globally unified trend of adoption in the UBI market is proof of concept. UBI-driven policies will touch the $115 billion mark in 2026, having grown at a CAGR of 21%. If you believe that UBI is still a concept for the future, the recent numbers will give you a more informed perspective – in 2018, UBI-paired policies contributed premiums worth $15 billion globally.

{kind=link}

- UBI and Telematics Can Help You Control the Risk Factors.

Market-traction might not always be the intuitive reason why companies take up new product strategies. UBI is as much a risk-management tool as it is a new product category.

Platforms like Kruzr are able to gauge metrics that were earlier not even included in the policy documentation. Policy-holders that have Kruzr app installed on their phone are communicating data hard-braking data in real-time. Insures can now have a better understanding of such strong indicators that describe the associated risk at a greater length and also have strong predictive powers.

Kruzr goes beyond the risk-measurement and helps the insurance companies mitigate risk. University of British Columbia researchers showed a 21% decline in hard-braking behavior after users opted for policies operating on UBI and telematics. A similar trend is visible in the enterprise space. Willis Towers Watson’s research showed an 80% drop in crashes among fleets managed using telematics solutions.

Built on this insight, Kruzr’s app nudges the driver whenever she starts exhibiting risky or drowsy behavior. Insurers who are working only with risk parameters are able to price the risk into the policy, but if too many claims start coming in, it would be a disaster as big as the ones faced by companies working with not-so-robust risk management programs. Hence, Kruzr ensures that risky behavior is mitigated right when the probability of risky behavior starts going up.

- Efficient Product Engineering with Solutions that Tackle a Wide Range of Problems.

An easy way to launch a product that can drive a company into liquidity or solvency issues is by investing significant capital into it before the product is even brought to market. Insurance companies like Mission and Transit faced a similar issue because a large portfolio of their products was run by the brokers and agents. By the time the product reached the end-user, it was already carrying the weight of overheads.

The Kruzr team worked on the problem right at the outset. With a readily available Software Development Kit, any insurance company can develop a white-label solution on top of the Kruzr platform. This reduces the go-to-market time and shrinks the cost of development, testing, and deployment to its lowest denominator. And all of this works, even as the Kruzr technology provides a better grip on the risk parameters and a more innovative set of UBI products.

Conclusion

No one would say Nokia, Mission, or Transit did not innovate or expand. However, it is not difficult to conclude that the direction of their investments in innovation was not quite right. While an insurance business should stay away from such existential risks, it cannot entirely skip cycles of innovation. Eventually, every insurance business has to stay ahead of the curve and adopt relevant technological innovations.

Kruzr brings an all-encompassing set of solutions in the form of its AI engine, comprehensive risk assessment platform, predictive analytics, and driver-behavior nudges. When integrated with the right insurance product portfolio, Kruzr can make the missing piece of your innovation puzzle.